Portable vs. Assumable Loans: The Next Big Shift in Home Financing?

What’s driving the discussion

The housing market right now is facing a familiar but tough challenge: many homeowners are “locked in” with very low interest rates (say 3 % or lower) while new borrowers face much higher rates (5-6 %+). This creates a strong disincentive for people to move: if you sell, you will take on a new mortgage at a much higher rate, even if you really want to relocate.

To help address this, the Federal Housing Finance Agency (FHFA) — which oversees the major mortgage-backed securities buyers Fannie Mae and Freddie Mac — has publicly stated it’s evaluating two specific ideas: assumable mortgages and portable mortgages/loans. In short:

-

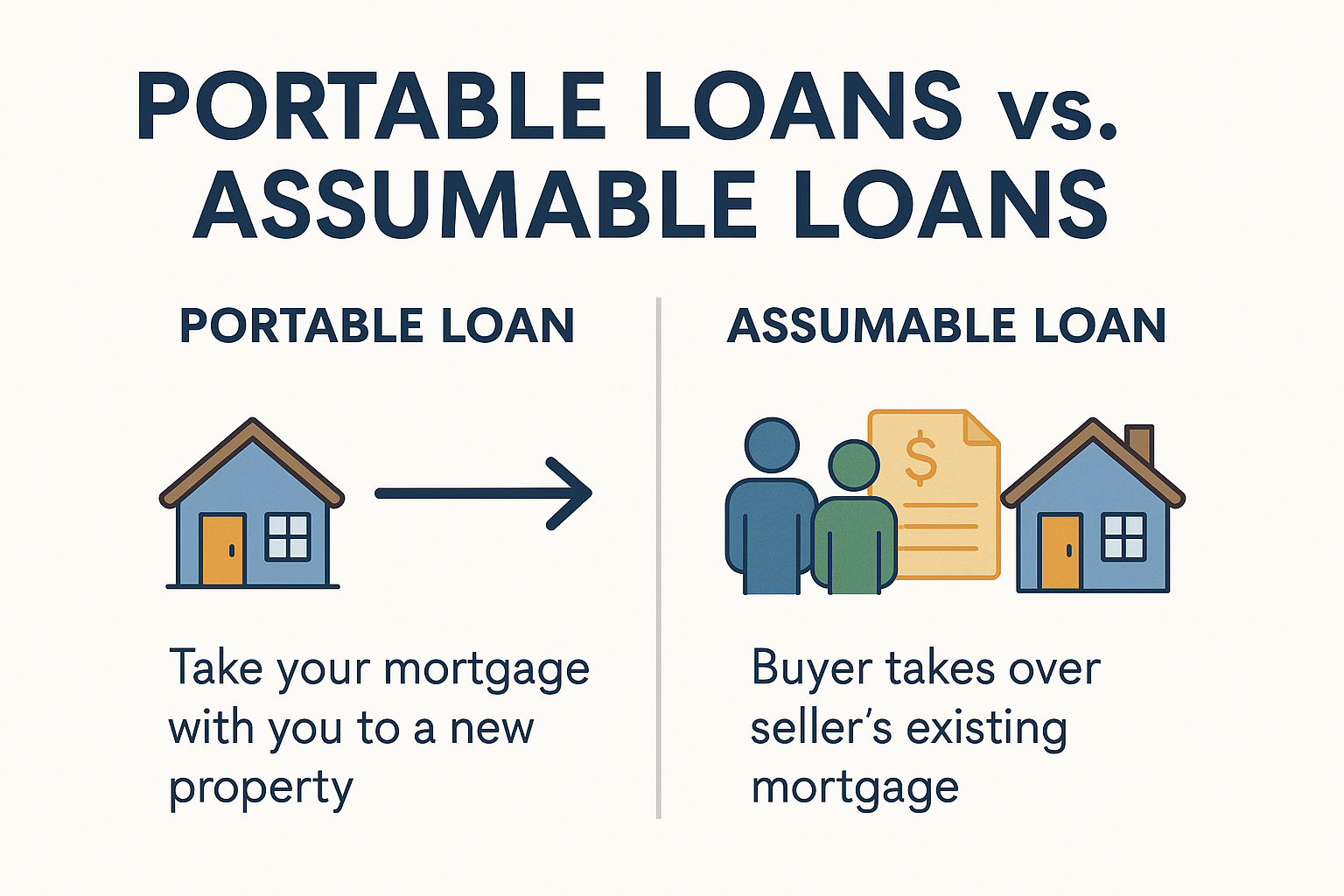

Assumable loan: A buyer takes over a seller’s existing mortgage (rate, term and balance) under certain conditions.

-

Portable loan: A homeowner carries their existing mortgage terms to a new property when they move.

Defining the terms

Assumable mortgages

An assumable mortgage allows a homebuyer to “assume” (take over) the seller’s loan — keeping the existing interest rate and term (and often remaining balance) instead of originating a new loan at the current market rate. The seller’s loan essentially becomes the buyer’s loan (after underwriting and approval).

These already exist in specific U.S. loan products (for example, many of the government-backed loans such as those by the Federal Housing Administration (FHA) or U.S. Department of Veterans Affairs (VA) are assumable).

Portable mortgages / loans

In a portable loan scenario, a borrower who holds a mortgage would be able to carry that same mortgage (including its rate, term, structure) when they move from one property to another. So instead of paying off their existing mortgage and taking out a new one, they “port” the old loan to the new home. This concept is common in some other countries (e.g., Canada) but has not been widely used in the U.S. residential market.

The key difference:

-

Assumable: The buyer takes over someone else’s loan.

-

Portable: The borrower keeps their loan but moves it to a new property.

How they compare — key differences

| Feature | Assumable Loan | Portable Loan |

|---|---|---|

| Who benefits | Buyer of a home with a low-rate existing loan | Existing homeowner who wants to move and keep their low-rate loan |

| What remains unchanged | Rate and term of seller’s loan (after underwriting) | Rate and term of original loan remain with borrower when moving |

| When it applies | At sale of property where loan exists | When borrower sells old home and buys a new one |

| Main challenge | Buyer must qualify for assumption and may need to cover equity gap | Loan is tied to original property; transferring collateral adds complexity |

| Impact on housing mobility | Helps buyers access low rates | Helps homeowners move without giving up low rates |

| Secondary market / investor concerns | Existing loan stays in place, limiting new originations | Changing collateral complicates securitization and servicing |

Why this matters now

Several factors make this discussion timely:

-

Many homeowners locked in at very low interest rates are reluctant to move. They effectively lose a favorable mortgage if they sell. This “lock-in effect” reduces housing mobility and inventory.

-

Mortgage rates remain elevated relative to recent historic lows, so moving often means taking on a higher rate. An assumption or portability can provide a competitive advantage.

-

The FHFA’s interest signals a policy push to expand tools that might ease affordability/mobility.

-

For the industry (lenders, servicers, secondary markets): these innovations would impact origination volumes, servicing portfolios, investor risk profiles, and loan-pool structures.

Potential benefits

Here are some of the upsides if these ideas can be made practical:

-

Better mobility for homeowners: A homeowner with a low rate might move without penalty of a higher new rate (thanks to portability).

-

Affordability help for buyers: A buyer assuming a loan at, say, 3 % when new mortgages run 6 % can meaningfully reduce monthly payment and total interest cost.

-

More housing market fluidity: If homeowners feel freer to sell/move because they aren’t locked in by their low rate, inventory may increase and mis-allocations decrease.

-

Potential for sellers as differentiators: Sellers with low-rate loans might market the fact that their buyer can assume the loan — giving them an edge.

-

Servicer/Investor benefits: Some servicers may prefer loan assumptions rather than payoff and churn. For example, keeping servicing rights and avoiding payouts.

Significant challenges & risks

However, there are many caveats and hurdles:

-

Underwriting and credit risk: For assumptions, the buyer still must qualify. The economic benefit might tempt weaker borrowers or stretch underwriting standards.

-

Secondary market/servicing complications: Especially for portable loans, the fact that the loan moves to a different property means the collateral backing the loan changes — this complicates pooling, securitization and the modeling of risk.

-

Loan economics and incentives: Lenders and investors may get less newer originations or get locked into lower-yield assets if many loans become available for assumption/portability. Some in the industry question whether the incentives work.

-

Equity gap and second liens: In an assumption, if a seller’s loan balance is much lower than current market purchase price, the buyer must make up the gap (either with down payment or second mortgage). That reduces the benefit.

-

Legal/contractual obstacles: Many U.S. mortgages are tied by collateral to the original property. Porting the note to a new property would require substantial structural and legal change.

-

Impact on first-time homebuyers: There’s concern that increasing options for mobility or assumption/portability may raise home prices (by increasing purchasing power) and thereby make it harder for buyers without existing low-rate loans.

What this means for different stakeholders

For homebuyers

If you’re buying a home and see a property where the seller’s existing low-rate loan is assumable, that could be a major financial benefit. But you’ll need to:

-

Check that the loan is eligible to be assumed (not all loans are).

-

Qualify in underwriting to take over the loan.

-

Be prepared to cover the equity gap (if the property price is much higher than the remaining loan balance).

If you don’t have that opportunity, then portable loans won’t immediately help you — since portability helps the owner moving, not the buyer without an existing loan.

For existing homeowners thinking of moving

If a portability option becomes available, you might be able to keep your low-rate mortgage when you move — which would reduce the penalty of moving. But you’ll need to watch for:

-

How the new program handles collateral change and property value difference.

-

Whether you must re-qualify/underwrite anyway.

-

Whether the new home cost is significantly higher, necessitating additional financing or second lien.

-

Whether the feature is retroactive (unlikely) or only applies to new originations/loans under new rules.

For lenders, servicers and investors

There’s a balancing act: On one hand, offering assumability or portability can be a competitive differentiator; on the other hand, it may reduce the volume of new originations, keep lower-yield assets in portfolios longer, or complicate servicing and securitization. Industry commentary suggests this is a major hurdle.

In addition, operational and systems changes (tracking, underwriting, documentation) will be needed.

For the housing market and policy side

From a policy viewpoint, unlocking mobility and unlocking low-rate loans could be a lever to improve affordability and inventory — but affordability doesn’t depend only on rate. If home prices rise or if the benefit is not widely accessible (e.g., mostly to those already holding low-rate loans), the net effect may be limited. Some commentators argue that “portable mortgages don’t work in the U.S.” at scale because of structural differences.

Also, widespread portability or assumption could impact the mortgage-backed securities market in unanticipated ways.

Bottom line: where we’re at & what to watch

-

The FHFA has publicly signaled that it is evaluating (but has not yet committed to) expanded assumable or portable mortgage programs.

-

Assumable mortgages are the more “ready” of the two: they already exist (in limited form) in the U.S., and expanding eligibility may be more feasible.

-

Portable mortgages are conceptually attractive but face major structural/legal/market hurdles in the U.S. context (because of how mortgages are tied to property collateral, how fixed-rate long-term loans dominate, etc.).

-

For a typical borrower: If you’re buying a home and find one with an assumable low-rate loan, that could be a big win. But if you don’t hold a low-rate loan now, portability may not help you for a while (if at all).

-

It's worth staying alert: If new rules are announced, lenders may begin to roll out products, and real-estate agents/brokers will need to understand how to market/qualify these.

-

But important caveat: Even if implemented, these tools are not a silver bullet for affordability. They won’t automatically lower home prices or fix supply side constraints. They mainly shift financing dynamics for a subset of borrowers.

Final thoughts

In a nutshell: The emerging proposal to enable more broadly assumable loans and possibly portable loans is a potentially important development for the U.S. housing system — especially given the current interest-rate/lock-in environment.

But the devil is in the details: how the programs are structured, who qualifies, how the industry and secondary market respond.

If you’re a homeowner, know that this could open up new possibilities for moving with your low rate intact; if you’re a buyer, look out for homes where the seller’s existing loan may be assumable. And if you’re in the real-estate/financing business, be ready for systems and underwriting changes if this gains momentum.

Ultimately, though, this is one piece of a much larger housing-affordability puzzle. Financing innovations help—but they don’t replace the need for more inventory, better wage/rate alignment, and broader economic support.

Ready to Take Advantage of Portland’s Buyer’s Market?

📞 Schedule a quick 30-minute call: HERE

📧 Or e-mail me directly to start your Portland home search at brian.valdez@exprealty.com

Categories

- All Blogs (9)

- 50-year mortgage (1)

- Builder Incentives (1)

- Buyer Education / First-Time Homebuyers (6)

- Home Buying Tips & Insights (5)

- Home Financing & Mortgage Education (3)

- Housing Affordability (5)

- Negotiation Strategies (2)

- Portland Neighborhoods (3)

- Portland Real Estate Market Updates (4)

- Real Estate Market Insights (6)

- Real Estate News & Policy (6)

- Renting (1)

Recent Posts

Oregon REALTOR®, eXp Realty | License ID: 201260392

+1(503) 503-0446 | brian.valdez@exprealty.com